Can Breast Cancer Survivors Get Term Life Insurance?

The answer is yes, but the availability and cost of life insurance will depend on the stage of your cancer, the treatment received, and your current health.

Cancer is a high-risk condition. At RiskQuoter, we specialize in helping women find the best life insurance after breast cancer.

Breast Cancer Life Insurance Overview

Breast cancer is the second-leading cause of cancer death among women.

It’s one of the most common types of cancer among women, and in general, its incidence rate has been steadily increasing.

In light of these statistics, it’s no surprise that many people are concerned about how a breast cancer diagnosis might impact their ability to secure life insurance coverage.

Breast cancer underwriting factors include:

- The type of breast cancer you had

- Cancer stage

- Treatment received

- Time since completing treatment

- Other cancer histories – Thyroid, kidney, etc. Basal cell skin cancer is not problematic.

We specialize in cancer life insurance and will help you find affordable insurance from top-rated companies.

We use a quick quote process that allows us to shop life insurers quickly for underwriting feedback.

The benefit of a quick quote is that you’ll receive preliminary quotes upfront before you complete an application.

Client Reviews

Michael was extremely helpful and courteous while working with us to get the best life insurance policy for our family. Thank you!

Kaitlyn G.

The best service and the best rates, Thanks for all the help!

Elizabeth C.

I was very pleased with the attention and personalization I received while working with Mike. It definitely made the process of finding the right policy easier.

Tina H.

How Does Breast Cancer Affect Life Insurance?

After you complete all treatment, most life insurers postpone offering coverage for a while.

A flat extra charge is added to your price after the postponed period.

While flat extras are temporary (3-5 years), they are expensive and add $600 – $1,000 per every $100,000 coverage.

For most breast cancer survivors, a “standard” or possibly a “standard plus” is the best rate that will ever be available.

Life Insurance Underwriting for Breast Cancer Survivors

The cancer stage is the starting point for life insurance companies.

While many other factors impact life insurance underwriting, all carriers start with the breast cancer stage.

Other significant health issues like Crohn’s or ulcerative colitis can affect your rate, while minor issues like elevated cholesterol have little impact on underwriting.

Remember that the following are general guidelines: every cancer history is uniquely different.

Your best breast cancer life insurance company will depend on your medical history.

Stage Zero Breast Cancer Life Insurance

Stage zero breast cancer (the earliest form) is called ductal carcinoma in situ (DCIS).

Life insurance is available 3-6 months after completing treatment.

The best place to start is with a copy of the pathology report, as slight variations result in significantly different underwriting outcomes.

We need the following details about your DCIS history:

- What type of DCIS did you have?

- DCIS

- DCIS with micro-invasion

- Invasive DCIS

- What was the DCIS Grade?

- Low grade (grade 1)

- Moderate grade (grade 2)

- High grade (grade 3)

- What was the hormone receptor status?

- Estrogen Receptor (ER) positive or

- Is Estrogen Receptor negative?

- How was the DCIS treated?

- Lumpectomy

- Lumpectomy and radiation

- Mastectomy

- Hormone therapy (Tamoxifen, Arimidex, Aromasin)

The above factors determine when life insurance is available.

You may get a “standard” or “standard plus” rate with some companies.

And while some medications may elevate liver enzymes or increase the risk of stroke, it doesn’t typically affect underwriting.

If you had lobular carcinoma in situ (LCIS), the same underwriting rules as DCIS would apply.

DCIS Client Life Insurance Success Story:

- Age 49 at the time of diagnosis

- The mammogram detected a lump.

- Biopsy confirmed DCIS

- A lumpectomy was completed, and surgical margins were negative.

- Cancer tested ER-Positive.

- Radiation treatment for three weeks after surgery.

Her only other medical history was medication for generalized anxiety.

Prudential offered the best rate for this client at a non-smoker plus (standard plus) final offer. We were able to get her an affordable term life insurance policy.

Stage 1 Breast Cancer

Most Stage 1A and Stage 1B cancers are insurable within 3-6 months of treatment.

The following weigh more favorably in underwriting:

- Stage 1A or Stage 1B breast cancer

- Low-Grade tumors

- Age 40 or older at the time of diagnosis

- Tumor size is 10 mm or less in size

- Estrogen Receptor-Positive (ER-Positive)

- No lymph node involvement

- No family history of breast cancer with mothers.

- No history of heart conditions, gastrointestinal, hepatitis, or diabetes.

Stage 1c breast cancers follow the underwriting rules for stage 2 cancers, as mentioned later in this article.

Stage 1 Breast Cancer Life Insurance Outcomes

If your breast cancer is ER-Positive, standard life insurance rates are possible.

If not ER-Positive, most insurers will postpone offering life insurance for 1-2 years after all treatment.

A temporary flat extra (3-5 years) of $500-$750 per every $100,000 life insurance is added to the standard rate.

If your cancer was stage 1C breast cancer, please follow the guidelines for Stage 2 cancers mentioned below.

Stage 2 Breast Cancer

Stage 2 breast cancers require a postponed period before life insurance will be available.

The waiting period depends on factors such as:

- Was the cancer Stage 2A or 2B?

- What was the size of the tumor?

- Were any lymph nodes positive for cancer?

- If yes, how many and where were they located?

- HER2 status – was the tumor positive or negative?

- ER-Positive – was the tumor estrogen receptor-positive?

- Was the tumor progesterone receptor positive or negative?

- Was an Oncotype DX Score completed? If yes, what was the score?

Stage 2A breast cancers typically require 5-year waiting periods after completing all treatment.

Stage 2B breast cancers require 5-10 years before life insurance is available.

Best Case Scenario for Stage 2 Breast Cancers

When life insurance is available, it’s common to see underwriting offers as follows:

Stage 2A Breast Cancer

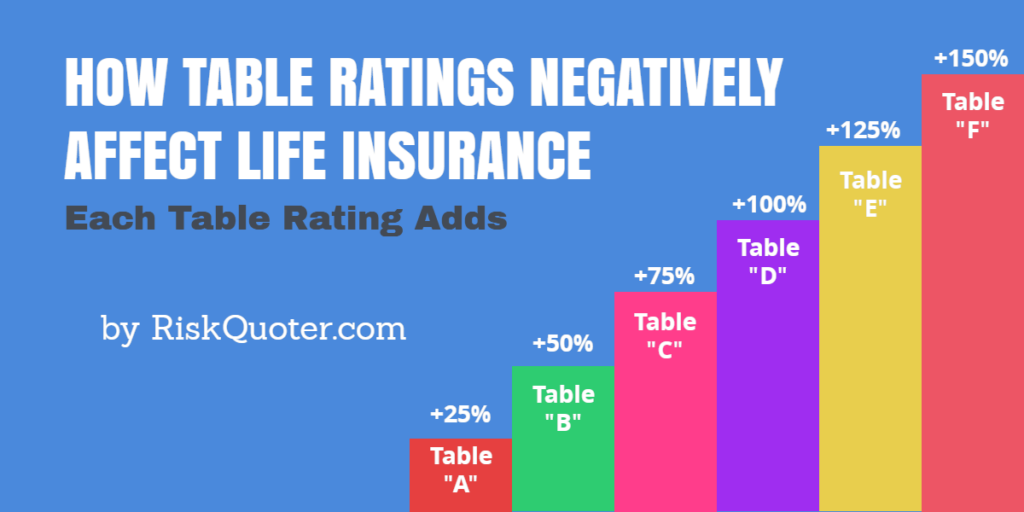

Standard rates plus a table rating and a flat extra will apply.

The table rating is permanent and adds 50% to standard rates.

The temporary flat extra will add $1,000 – $1,500 for every $100,000 coverage you apply for.

Stage 2B Breast Cancer

The difference between Stage 2A and 2B cancers is the length of time that the flat extra will last.

Stage 3 breast cancers

Stage 3 breast cancer requires postponed periods of 10-15 years.

Life insurance is case-by-case.

Best-case scenarios require a 50-100% table rating and a flat extra expense.

The flat will add $1,500 – $2000 for every $100,000 in life insurance.

Stage 4 breast cancers

The type of life insurance available for stage 4 breast cancers is limited to guaranteed issue life insurance policies.

Survivorship policies can have one uninsurable person.

Recent Articles:

Get the Best Life Insurance Table Rating for Your Situation

Top 10 Health Problems in America

Kidney Cancer Survivors – Life Insurance is Available!

If you’ve had kidney cancer and need life insurance, we can help you. Finding life…

Life Insurance for Throat Cancer Survivors

We specialize in high-risk life insurance underwriting for throat cancer survivors. While head and neck cancers…

How to Get Life Insurance after Colon Cancer

When you have colon cancer, the last thing on your mind is probably getting life…

Addison’s Disease Life Insurance

If you have Addison’s Disease and need life insurance, let us help you. Our life…

Breast Cancer Life Insurance Underwriting Questions

Underwriters need to know:

- What type of breast cancer did you have?

- When were you diagnosed with breast cancer?

- What kind of treatment did you receive?

- When did you start and finish all therapy?

- Stage of breast cancer?

- What is the grade of the cancer cells?

- What was the size of the tumor?

- Were surgical margins positive, negative, or close?

- Were any lymph nodes positive for cancer?

- If yes, how many and where were they located?

- Were breast cells hormone receptor-positive or negative?

- Did you have genetic testing?

- If yes, what test and what were the results?

- Have you had any breast cancer recurrences?

- Do you take any medications? If yes, what do you take?

- Is there any family history of breast cancer?

- Have you been diagnosed with or treated for:

- mental health – bipolar, depression, anxiety?

- respiratory – asthma, sleep apnea

- brain – epilepsy, multiple sclerosis

- endocrine – diabetes, metabolic syndrome, proteinuria, and thyroid disease.

It’s important for us to know about any genetic testing that was completed as it could help your life insurance underwriting.

The most common breast cancer gene test is the BRCA genetic test.

Don’t worry if you do not have all the answers to the following. We’ll work with the information you have available.

Declined or Rated Due to Breast Cancer?

Have you been denied life insurance due to breast cancer?

Some of the common misconceptions about life insurance for breast cancer survivors include:

- If one company declines me, they all will – FALSE

- Ratings will be the same with each company – FALSE

- The waiting period is the same with all life insurers – FALSE

- My agent told me the offer I received was the best – Maybe

Of the 100+ life insurers in America, less than 10 of these companies specialize in life insurance for breast cancer survivors.

We can help you with our underwriting expertise.

We’ll help you find the best life insurance companies based on your individual breast cancer history.

FAQ

You have questions about life insurance after breast cancer, and we have the answers.

Final Words

Remember to re-shop the market each year when a flat extra is involved.

Especially now that COVID has affected underwriting rules.

The reason is that underwriting offers tend to improve as more time passes since breast cancer.

First off, there is never any pressure or obligation with our service.

You get the information you need to make an informed decision about life insurance for you or a spouse.

Please take a few minutes to request your quote today.

Related Articles