Life insurance is already confusing enough.

Then you hear the words “table rating” — and suddenly your costs are way higher than you expected.

The good news? You don’t have to settle. We’ll help you find the right life insurance company – and the right policy – so you get the best rates, even if you’ve been rated before.

In this guide, you’ll learn:

- What life insurance table ratings are

- How much do they cost you

- How to reduce or eliminate them

- Real examples of how we help clients save thousands

Let’s dive in.

What are Life Insurance Table Ratings?

A life insurance table rating is a surcharge that companies add when they believe you are a higher risk.

- It could be due to:

- Health Issues

- Dangerous Jobs

- Risky Hobbies (like scuba diving or private flying)

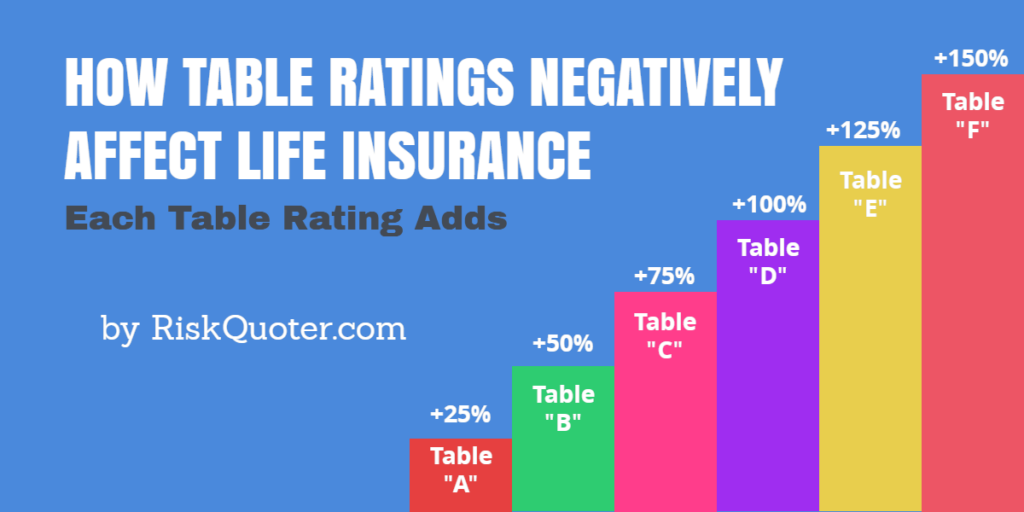

Ratings are typically labeled 1-16 or A-P, and each rating corresponds to a 25% increase in the standard rate.

Major health issues, such as heart conditions, significant cancer history, or gastrointestinal conditions, receive ratings, while minor health issues, such as high blood pressure or high cholesterol, do not.

How Much Table Ratings Cost (and Why It Matters)

Here’s a quick look at how ratings increase your price:

| Table Rating | % | Rating Cost | Total Rate |

|---|---|---|---|

| 1 (A) | 25 | $125 | $625 |

| 2 (B) | 50 | $250 | $750 |

| 3 (C) | 75 | $375 | $875 |

| 4 (D) | 100 | $500 | $1000 |

| 5 (E) | 125 | $625 | $1125 |

| 6 (F) | 150 | $750 | $1250 |

| 7 (G) | 175 | $875 | $1375 |

| 8 (H) | 200 | $1000 | $1500 |

| 9 (I) | 225 | $1125 | $1625 |

| 10 (J) | 250 | $1250 | $1750 |

| 11 (K) | 275 | $1375 | $1875 |

| 12 (L) | 300 | $1500 | $2000 |

| 13 (M) | 325 | $1625 | $2125 |

| 14 (N) | 350 | $1750 | $2250 |

| 15 (O) | 375 | $1875 | $2375 |

| 16 (P) | 400 | $2000 | $2500 |

- Example:

- Standard premium – $500 per year.

- Table 2 (B) increases the cost by 50% ($250), so the price would now be $750 per year.

And that’s just with a $500 base rate. Imagine if you were buying $ 1M+ coverage — the impact could be huge.

Are Table Ratings Negotiable?

Short answer: not really.

Life insurance underwriters follow internal guidelines and those of their reinsurers. You may occasionally be moved down one table if you have other positive health factors, but this is rare.

It’s often easier to move you to a new company for a better rate than to try to renegotiate your offer with the existing company.

How Table Shave Programs Help Lower Costs

Some insurers offer special “table shave” programs that reward applicants for making positive changes to their health.

Here’s what’s available:

| Company | Program Details |

|---|---|

| Banner Life | One rate class improvement if you meet 3 of 7 credit criteria. |

| Corebridge Financial | Expanded Standard – Up to Table 2 rating gets a standard rate on UL policies Flex Points Crediting Programs – One rate class improvement if you meet 4 of 16 crediting criteria. |

| John Hancock | Vitality Program – Better rates for ongoing sharing of health information |

| Lincoln Financial | Table Reduction – Table 3 reduced to Standard rate – UL policies |

| Minnesota Life | Mortality Credits – One rate class improvement for all products. |

| Pacific Life | Healthy Rewards – Holistic underwriting approach to improve rates. |

| Principal | Principal Risk Upgrade Program (PRUP) – Table 2 to Standard – all products Healthy Lifestyle Credits – One rate class improvement – all products |

| Protective | Pro Credit – Standard to Preferred program |

| Prudential | Underwriting Credit Opportunities – Rate class improvement for two dozen health issues. |

Most of the above credit programs are designed to help people with mild health impairments who have taken positive steps since their diagnosis. Cases that have flat extra ratings may also qualify for these programs.

Medical Conditions That Usually Get Rated

Here’s a rough guide based on various health conditions of what to expect.

Cancer History Table Ratings

If you have a history of cancer, tables are typically only used when the cancer stage is stage T2b or greater. Here are some examples:

| Condition | Typical Rating Range |

|---|---|

| Bladder Cancer | Table 2 range, flat extra possible |

| Breast Cancer | Stage T1c or greater will have a table rating and flat extra. |

| Colon Cancer | Stage 2 or greater will have a table rating. |

| Kidney Cancer | Stage 2 or greater = table rating |

| Melanoma | Stage 3 melanoma will have a table rating. |

| Prostate Cancer | Stage T2c or greater = table rating plus flat extra |

It is important to note that these guidelines are general, and as more time passes, we may be able to find companies willing to underwrite you without an additional fee.

Heart Conditions That Have Table Ratings

The history and extent of your heart condition determine if a rating will be necessary. Some examples include the following:

| Heart Condition | Typical Rating Range |

|---|---|

| High Blood Pressure | Table ratings are rare. If you have one, you’re with the wrong company |

| Aortic Stenosis | You will have a table rating |

| Atrial Fibrillation | Some mild cases may receive standard rates. |

| Heart Attack | Most cases start at Table 4, but may improve as more time passes |

| Heart Blocks | Mild cases don’t, moderate and severe cases will have a table rating |

| Mitral Valve | Most conditions will have a table rating. |

Gastrointestinal Table Ratings

- If you have a gastrointestinal condition such as any of the following, you may receive a table-rated offer:

- Hepatitis – Will almost always be table-rated unless it was successfully treated.

- Ulcerative Colitis – Moderate and severe cases are rated, while mild cases may not be.

- Crohn’s Disease – Same as ulcerative colitis.

- Elevated Liver Tests – Ratings depend on the degree of elevation and the extent of underlying damage.

Other Medical Conditions and Table Ratings

Here’s how underwriting views the following conditions:

- HIV Positive – There is always a table rating.

- Sleep Apnea – Table ratings are rare unless there is non-compliance with CPAP.

- Mental health conditions – Anxiety is not rated for most, but bipolar disorder is rated.

- Epilepsy – Most cases will receive some form of table rating.

- Multiple Sclerosis – Table ratings get progressively worse as MS progresses.

- Stroke History – Most are rated, but a TIA history may not be.

Should You Accept a Rated Offer?

Here’s our recommended play:

- Accept the offer temporarily

- Lock in protection now

- Reshop for a better offer

- Switch if better rates appear

We recommend this because your current offer may be the best available, and you don’t want to miss out on it if that’s the case. We can always replace it if we find a better offer.

Your options include the following:

- Decline the Offer

- Accept the Offer

- Temporarily accept the offer

- Reduce the Coverage/ Change the Terms

In most cases, it is best to accept the offer temporarily. We’ll then re-shop the market for you to see if better offers are available.

You can switch to the new company if we find a better offer.

If not, you will have coverage if all other companies deny you life insurance.

Final Words: Beat Table Ratings with the Right Partner

Our expertise is life insurance underwriting. We use a quick quote approach to determine which life insurance company is best for you quickly.

The benefit to you is that you’ll know which company is best suited for you before you apply for coverage.

Ready to get started?

Submit your request for life insurance quotes today!