Don’t let an aortic valve disorder like aortic stenosis or regurgitation stop you from getting affordable life insurance.

This guide provides the information you need to make an informed decision about whether you have aortic stenosis, regurgitation, or other valve diseases.

Underwriting Tip

Aortic stenosis and aortic regurgitation can worsen over time. Get coverage today before it gets more expensive!

Aortic Stenosis Life Insurance: Understanding Your Options

Aortic valve stenosis occurs when the valve between your aorta and heart chamber is narrowed and doesn’t open fully.

The Mayo Clinic offers a complete medical review of this condition.

It may be congenital, such as a bicuspid aortic valve, or acquired through calcification, degeneration, or aging of the valve.

Less frequently, rheumatic fever or endocarditis may be the cause.

For many people, the first indication of aortic stenosis may come from their doctor when they hear a heart murmur.

An echocardiogram is then commonly used to evaluate the severity of the stenosis.

Symptoms of aortic stenosis may include:

- Heart murmur sounds

- Shortness of breath

- Fatigue

- Dizziness, fainting

You may not have symptoms unless the aortic stenosis becomes severe.

Severe cases may require valve repair (valvuloplasty) or replacement.

How Aortic Stenosis Impacts Life Insurance Underwriting

Aortic stenosis life insurance rates range from minimal impact to table rated or declined for severe aortic valve stenosis.

Fortunately, life insurers no longer add flat-extra expense ratings to policies.

Underwriting is based on your age and stenosis severity level. The following are general underwriting guidelines for aortic stenosis.

| Age | Mild | Moderate | Severe |

|---|---|---|---|

| 15-29 | Table 4-5 | Table 6-12 | Decline |

| 30-44 | Table 3-4 | Table 5-8 | Decline |

| 45-59 | Table 2-4 | Table 4-8 | Decline |

| 60-74 | Table 1-3 | Table 3-6 | Decline |

| 75+ | Standard | Table 2-3 | Decline |

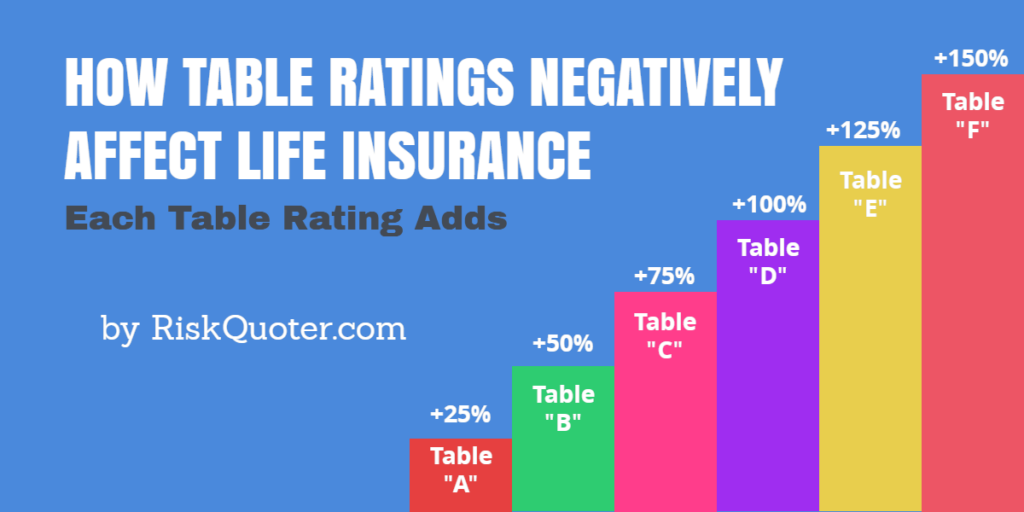

Each table rating adds approximately 25% to a standard rate, so table 2 would add 50%, and table 3 would add 75%, etc.

Other factors that may affect your life insurance rates include:

- Irregular heartbeat

- Atrial fibrillation

- High Blood Pressure, diabetes, stroke history.

- If you’ve had other significant health issues – ex. prostate cancer, diabetes, etc.

A related condition that affects underwriting is aortic sclerosis – a valve disease where the valve thickens and becomes stiff.

Tips for Getting Approved for Life Insurance with Aortic Stenosis

The best thing you can do for yourself is to complete all required cardiac testing, follow doctor’s orders, and have accurate information about your medical history.

We use a quick quote process for our clients with aortic stenosis.

A quick quote lets us summarize your health history and shop the competitive companies for your medical condition.

The benefit is that you’ll receive underwriting feedback in about 3 days from the companies that understand how to underwrite aortic stenosis.

We’ll tell you exactly what information is needed for accurate quotes.

Case Studies for Aortic Stenosis

Mild Aortic Stenosis – A confirmed diagnosis after an echocardiogram will result in underwriting offers in the standard plus – standard table 4 range.

Example: Male, age 45 for $1,000,000 – 20 year term annual premium – quotes as of 7-1-2024, rates vary by company

| Rate Class | Company “A” | Company “B” |

|---|---|---|

| Standard Plus | $1591 | $1755 |

| Table 2 | $2341 | $3255 |

| Table 4 | $3092 | $4405 |

As you can see there are wide variations in price by company, so it’s critical to use the quick quote process we mentioned to get the best rate.

Aortic Regurgitation Life Insurance: What You Need to Know

Aortic regurgitation (insufficiency) is a type of heart valve disease where some blood pumped out of the left ventricle, leaks backward.

Common causes of regurgitation are progressive degeneration of a bicuspid valve and degeneration of an aging valve from calcification and sclerosis.1

Symptoms that may develop over time include:

- Shortness of breath

- Palpitations

- Irregular heartbeat

Severe cases of aortic insufficiency may require aortic valve repair with a procedure called an annuloplasty or heart valve replacement.

How Aortic Regurgitation Impacts Life Insurance Underwriting

Underwriting for aortic insufficiency depends on the severity, age, and treatment received.

| Age | Mild | Moderate | Severe |

|---|---|---|---|

| 15-29 | Table 4-5 | Table 6-12 | Decline |

| 30-44 | Table 3-4 | Table 5-8 | Decline |

| 45-59 | Table 2-4 | Table 4-8 | Decline |

| 60-74 | Table 1-3 | Table 3-6 | Decline |

| 75+ | Standard | Table 2-3 | Decline |

Tips for Obtaining Coverage with Aortic Regurgitation

As mentioned, we use a quick quote process to get underwriting feedback in days from competitive companies for aortic insufficiency/regurgitation.

The benefit to you is that you’ll know which insurers are best before you apply for coverage.

Life Insurance After Aortic Valve Replacement: What to Expect

If your condition is severe enough, you may have to go through surgery to have your aortic valve replaced.

Underwriting for aortic valve replacement is difficult but not impossible.

The valves are either mechanical valves or biological (tissue-based) coming from a pig or cow.

The two primary surgery methods are open heart surgery and transcatheter aortic valve replacement (TAVR).

The TAVR method typically leads to a quicker recovery which in turn means that life insurance is available sooner.

Life insurance prices after valve replacement depend on your age, severity of condition, and type of valve used.

Companies postpone offering coverage for 6-12 months due to the increased risk of having a stroke or embolism.

John Hancock Aortic Valve Replacement Underwriting

John Hancock requires a 12-month postponement period, and will consider the following ratings 2:

| Age | Mechanical Valve | Tissue Valve |

|---|---|---|

| 0-19 | I.C. | I.C. |

| 20-39 | Table 8 | I.C. |

| 40-49 | Table 6 | I.C. |

| 50-69 | Table 4 | Table 4 |

| 70+ | Table 3 | Table 2 |

Corebridge Financial Aortic Valve Replacement Underwriting

Corebridge Financial underwrites aortic valve replacement after a shorter 6-month postponement period.

| Age | Rating |

|---|---|

| Less than 40 | I.C. |

| 40-49 | Table 10 |

| 50-59 | Table 8 |

| 60-69 | Table 5 |

| 70+ | Table 3 |

Other factors like your heart’s ejection fraction percentage are considered. An ejection fraction of less than 50% is a decline.

If you have other health issues such as cancer history, diabetes, or other significant high-risk health issues, it’s almost impossible to get coverage.

Prudential Aortic Valve Replacement Underwriting

Prudential does well underwriting valve replacements and will consider coverage after a 12-month postponement period 3:

| Age | Rating |

|---|---|

| Less than 25 | Decline |

| 25-39 | Table F (6) |

| 40-49 | Table E (5) |

| 50-59 | Table D (4) |

| 60-69 | Table C (3) |

| 70+ | Table B (2) |

The above ratings assume favorable cardiac workups and no further issues related to the heart valve. This same underwriting table is used if you had mitral valve replacement surgery.

Frequently Asked Questions About Life Insurance with Aortic Valve Disease

Final Thoughts

Living with aortic valve disease doesn’t have to mean missing out on life insurance.

While getting approved might take a bit more effort, affordable options are out there for you.

We specialize in helping individuals with health conditions find the right coverage at affordable rates.

Request your quote today and let us help you secure the financial protection your family deserves.

Recent Articles: