You can get affordable life insurance if you have sleep apnea.

Sleep Apnea Overview

Obstructive sleep apnea is the most common type and the main focus of our life insurance underwriting.

An estimated 12 million Americans have sleep apnea.

At RiskQuoter, we’ve been helping clients for years.

Underwriting Sleep Apnea – How it Works

If you have obstructive sleep apnea, life insurance underwriters want to review your Polysomnogram.

Your life insurance price is based on your Polysomnogram test results and other medical risks.

Sleep apnea tests evaluate:

- Respiratory Patterns

- Chest Muscle Activity

- Oxygenation

Several high-risk life insurance companies will do well underwriting your obstructive sleep apnea history.

The best-case underwriting scenario for most people with obstructive sleep apnea is “standard” life insurance rates,

Although there are a few companies that will consider better rates if everything else about you meets their guidelines.

Underwriting Questions for Sleep Apnea

Here’s what we need to know about your sleep apnea history.

- Your age at the time of diagnosis of obstructive sleep apnea?

- How is your Sleep Apnea being treated? Observation, CPAP machine, Weight Loss, Surgery, other?

- Are you taking any medications for your obstructive sleep apnea?

- What are your height and weight?

- What is your blood pressure?

- Do you suffer from depression?

- Do you smoke?

- Have you had any other health problems?

Let us know if you have any heart disease, such as a heart attack history, aortic stenosis, etc. as that is a concern for underwriting.

Please note that if your medical records indicate that you should have a sleep study performed, which has not occurred, or your records indicate that you do not use your CPAP, most companies will postpone you until the test is complete.

FAQ

If you have questions about sleep apnea and life insurance, we have the answers!

Recent Articles:

No matter your health issue, whether it’s HIV, cancer history, heart disease, diabetes or any other condition, we can help you.

Get the Best Life Insurance Table Rating for Your Situation

Top 10 Health Problems in America

Kidney Cancer Survivors – Life Insurance is Available!

If you’ve had kidney cancer and need life insurance, we can help you. Finding life…

Life Insurance for Throat Cancer Survivors

We specialize in high-risk life insurance underwriting for throat cancer survivors. While head and neck cancers…

Life Insurance After Colon Cancer: A Step-by-Step Guide

Addison’s Disease Life Insurance

If you have Addison’s Disease and need life insurance, let us help you. Our life…

Sleep Apnea Life Insurance Rates

Obstructive Sleep Apnea is the most common type of sleep apnea.

From a life insurance underwriting standpoint, life insurance companies tend to offer their standard life insurance rates.

Occasionally, receiving a better life insurance rate is possible than the “standard.”

Not all life insurance companies will be competitive with underwriting obstructive sleep apnea.

Based on your specific obstructive sleep apnea circumstances, we know which life insurance companies are most aggressive.

Life insurance underwriters want to know what your Apnea Index is and what your Oxygen Saturation Levels are.

In addition, you must be compliant with your doctor’s orders.

Any additional medical factors that you can control, such as asthma, your build, weight, smoking, alcohol consumption, high blood pressure, etc.

This will affect your life insurance rates.

If your medical records indicate that you have taken steps to improve these areas,

This will help you from a life insurance underwriting standpoint.

How Apnea Index Affects Your Insurance Rate

Apnea Index of:

- 0-10 – typically, no additional life insurance cost

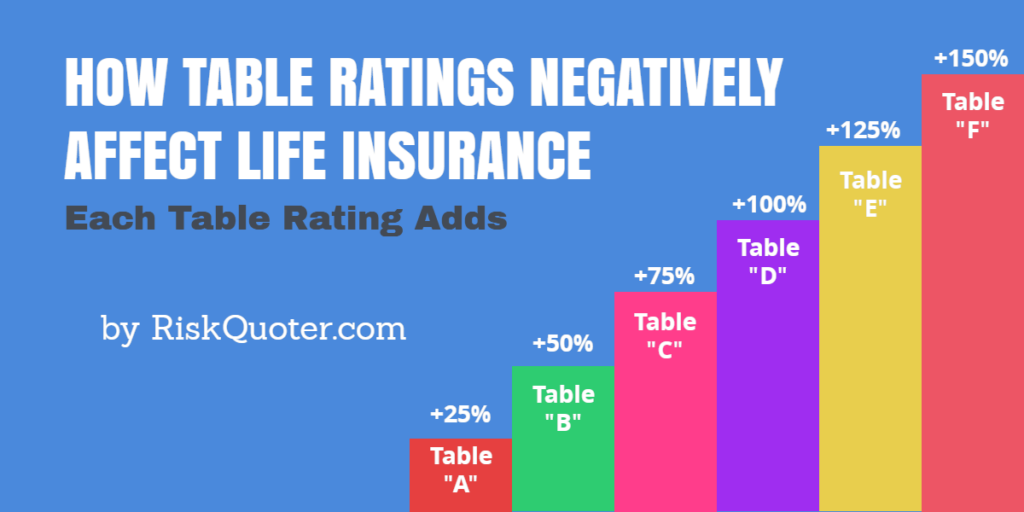

- 11-20 – 50% table rating increase over standard life insurance rates

- 21-30 – 100% table rating increase over standard life insurance rates

- 31-40 – 150% table rating increase over standard life insurance rates

- Above 40 – decline.

This assumes Oxygenation Levels in the 90% range.

Typically for every 10% decrease in oxygenation levels, life insurance companies will add a 25% table rating to the life insurance rates.

Table ratings typically increase the rate you pay 25% for each table assessed to your rate.

Mild, Moderate, and Severe Obstructive Sleep Apnea:

Is your sleep apnea mild, moderate, or severe?

Some possible life insurance ratings for your obstructive sleep apnea:

Mild Obstructive Sleep Apnea – Doesn’t require treatment.

The most likely scenario is a standard life insurance rate from life insurance companies,

Preferred life insurance rates may be possible with some life insurance companies.

Moderate Obstructive Sleep Apnea – Requires the use of a CPAP machine.

If you comply with doctor orders, the most likely scenario is “standard” to standard plus a 50% table rating increase.

If you are not compliant with doctor’s orders,

The most likely scenario is a 50% table rating increase over the standard rate to possible decline.

Severe Obstructive Sleep Apnea – Requires use of CPAP machine.

The most likely scenario if compliant is a 100% table rate increase over the “standard” life insurance rates.

If you are not compliant, most likely, you will be declined by life insurance companies.

Sleep Apnea Definitions

Sleep Apnea is caused by complete airway obstruction or a partial obstruction called Obstructive Hypopnea.

Obstruction occurs when the muscles in the upper part of the airway relax to the point that the airway collapses.

The Apnea Index – AI. The Apnea Index is a commonly used measure of the severity of obstructive sleep apnea during a sleep study.

The apnea index is calculated by dividing the total number of apneic events by the number of hours of sleep.

The higher the number, the more you will be charged for insurance.

Oxygen Saturation. A skin sensor measures oxygen saturation. Normal levels are greater than 90%.

Levels of less than 90% for a prolonged period typically indicate sleep apnea.

Chest Activity – The sleep study measures heart rate and patterns while sleeping.

Final Thoughts

Remember that these are sample underwriting guidelines, as every life insurance case differs.

We take the time to learn about your medical history.

We then shop your medical information to multiple life insurance companies to obtain the best possible rates.

There is never any pressure or obligation with our life insurance service.

We’ll give you the information you need to decide about your life insurance.

Please take a moment to complete our life insurance quote request.

Other health issues that we specialize in include:

- Gastrointestinal Conditions – Hepatitis, Ulcerative Colitis, Crohn’s Disease

- Cancer History – Prostate, Skin, Thyroid.