You may think that getting life insurance after testicular cancer is impossible, but at RiskQuoter, we’re here to let you know that you can get the life insurance coverage you need and deserve.

We help men with a history of testicular cancer find affordable term life insurance from top-rated carriers.

It’s never been easier for someone who has had testicular cancer to apply for coverage.

Testicular Cancer Overview

If you have had testicular cancer, you can get life insurance from a company that specializes in high-risk life insurance.

The most common type of testis cancer is seminoma.

Seminoma has two types: Classic and spermatocytic seminoma.

Nonseminomas are cancer cells that have different kinds of cells, including embryonal carcinoma, yolk sac carcinomas, choriocarcinomas, and teratomas.

In America about 9500 people get testicular cancer per year – it is not very common.

Does Life Insurance Cover Testicular Cancer?

Yes, several companies offer life insurance after testicular cancer.

Coverage may be available as soon as surgery (radical orchiectomy) has been completed.

Stage 1 Testicular Cancer

Life insurance is available for stage 1 classic seminomas as soon as treatment has been completed.

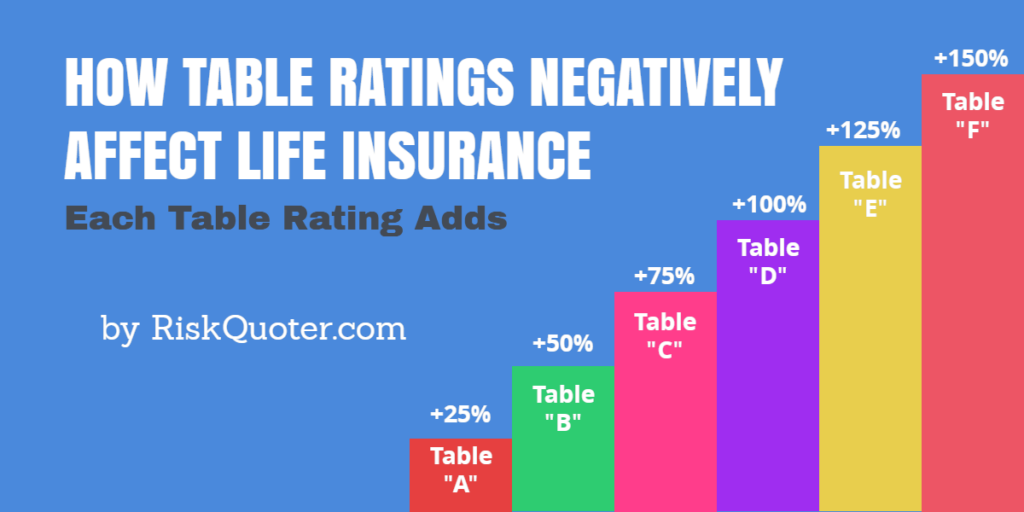

Current age under 60 – The first 3 years consist of “standard” rates plus a flat extra expense of $500 per every $100,000 of coverage. After 3 years, you pay “standard” rates for the rest of the policy.

Current age 60 or older – Companies charge the “standard” rate & flat extra, but one company does much better.

John Hancock will consider “standard” rates (no flat extra) from day one. It’s also possible to upgrade to “standard plus” rates after 5 years and “preferred” rates after 10 years.

Twelve-month postpone periods may be required if you had chemotherapy or radiation.

Stage 2 Testicular Cancer

Life insurance for stage 2 testicular cancer requires a postpone period of 0-24 months depending on your exact medical details.

Current age under 60 – The postpone period is typically 12-24 months, followed by “standard” rates plus a flat extra expense of $1,000 per every $100,000 for 4 years.

Current age 60 or older – John Hancock is still the best as they will consider standard rates plus the flat extra for 2 years. In some cases, they will even waive the flat extra entirely.

It’s important for us to get the exact dates of surgery, radiation, and/or chemotherapy in order to provide you with accurate quotes.

Stage 3 Testicular Cancer

Life insurance for stage 3 testicular cancers is on a case-by-case basis.

Most cases will require a minimum postpone period of 2-4 years.

Standard rates plus a 50% permanent rating will be added, plus a flat extra expense is likely.

Stage 4 Testicular Cancer

The only option available will be a guaranteed issue type of policy.

Graded benefit life insurance policies are available for age 40 or older.

Testicular Cancer Underwriting Questions

We use a quick quote process that gets you underwriting feedback in days from companies that specialize in cancer life insurance.

You’ll know which life insurance company is best before you apply for coverage.

Here’s what underwriters look for:

- When were you diagnosed with testicular cancer?

- How was the cancer treated? (surgery, radiation, chemotherapy)

- Did the cancer spread to any other parts of your body?

- Were any lymph nodes positive for cancer?

- Has there been any recurrence?

- Have you had the AFP or hCG tests completed?

- If yes, when and what were the results?

- Is there any family history of testicular cancer?

- Have you had any other health issues.

With the above, we can get you underwriting feedback in 3 days or less.

You’ll know exactly what to expect in terms of underwriting and price.

A note about tumor markers:

Early detection of testicular cancer uses the following tumor markers.

The key tumor markers are:

- AFP – alpha-fetoprotein (AFP) – normal = <5 ng/mlhCG

- hCG – human chorionic-gonadotropin (hCG) – normal = <5 ng/ml

Seminomas raise hCG levels but not AFP, while non-seminomas often raise hCG and/or hCG.

Final Words

Life insurance is possible after testicular cancer treatment.

We’ll help you find the best companies based on your individual health history.

Please take a few minutes to request a quote and we’ll contact you for the details regarding your cancer history. Thank you.

Recent Articles: