If you have a high-risk health history, we’ll help you find the best life insurance companies to meet your needs.

Don’t let a health issue stop you from getting affordable life insurance.

With RiskQuoter, we’ll match you with life insurers who understand health issues.

- Cancer Life Insurance

- Diabetes and Endocrine Disorders

- Life Insurance with Heart Conditions

- HIV Positive Life Insurance

- Gastrointestinal and Internal Organs

- Mental Health

- Prostate Disorders

- Respiratory

- Brain and Nervous System

- General Medical Conditions

- Tobacco and Nicotine Users

- Non-Medical Risks

- Get Your Best High-Risk Life Insurance Rate

- High-Risk Life Insurance Policies

- High-Risk Life Insurance Companies

- FAQ

- Final Thoughts

Cancer Life Insurance

We have excellent guides based on the type of cancer you had.

- Bladder Cancer

- Breast Cancer

- Cervical Cancer

- Colon Cancer

- Kidney Cancer

- Prostate Cancer

- Skin Cancer

- Throat Cancer

- Thyroid Cancer

You will find life insurance details by type of cancer, cancer stage, and treatment received.

Diabetes and Endocrine Disorders

Endocrine disorders require expertise to help you find your best life insurance rate, and that’s precisely what we do:

The above details everything you need to know to get affordable life insurance rates.

Life Insurance with Heart Conditions

The following is a general guide to getting life insurance for heart conditions.

Getting Life Insurance with Heart Conditions

The above guide includes information on heart conditions like:

- Abdominal Aortic Aneurysm

- Abnormal EKG

- Angina

- Angioplasty

- Atrial Fibrillation

- Bundle Branch Block

- Bypass Surgery

- Coronary Artery Disease

- Heart Attack

- High Blood Pressure

- Mitral Valve Prolapse

- Murmur

- Pacemaker

- Aortic Stenosis

You’ll find price ranges and expectations in the above guides.

HIV Positive Life Insurance

The following life insurance article gives you everything you need to know.

The above article details HIV underwriting by the company and provides sample rates from those companies.

Gastrointestinal and Internal Organs

The following articles detail how Inflammatory bowel diseases (IBD) affect your life insurance.

The above guide details underwriting, questions to expect, and the best companies by type of medical condition.

Mental Health

Find out what matters most to underwriters in the following article.

Life Insurance for Mental Health

This article covers anxiety, bipolar, OCD, suicide, and much more.

Check back often as we continually update the above mental health article.

Recent Articles:

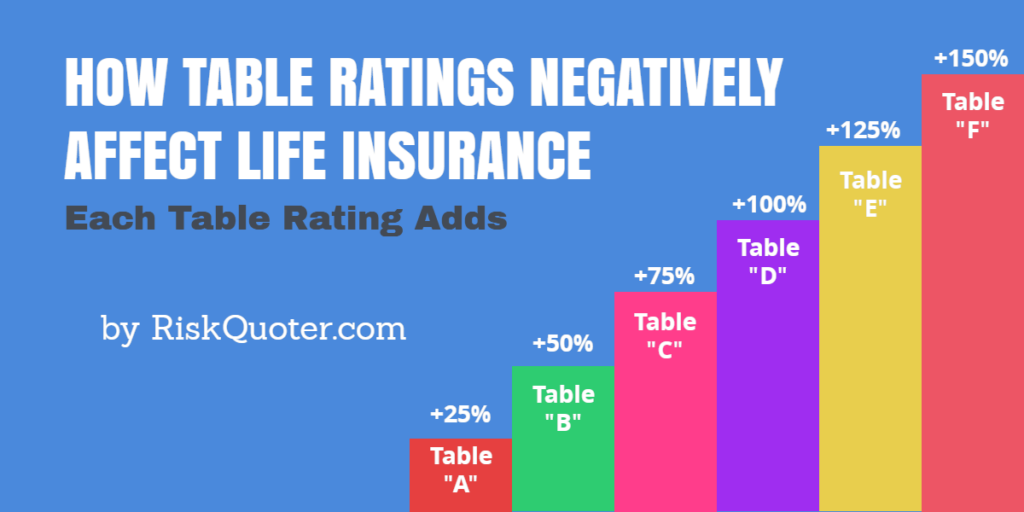

Get the Best Life Insurance Table Rating for Your Situation

Top 10 Health Problems in America

Kidney Cancer Survivors – Life Insurance is Available!

If you’ve had kidney cancer and need life insurance, we can help you. Finding life…

Life Insurance for Throat Cancer Survivors

We specialize in high-risk life insurance underwriting for throat cancer survivors. While head and neck cancers…

Life Insurance After Colon Cancer: A Step-by-Step Guide

Addison’s Disease Life Insurance

If you have Addison’s Disease and need life insurance, let us help you. Our life…

Prostate Disorders

We have some great companies that specialize in prostate disorders.

Prostate Disorders Life Insurance

The above guide covers:

- BPH

- Prostatitis

- PSA

- High-Grade PIN

- Low-Grade PIN

Underwriters want to know about your PSA history and biopsy results when determining your life insurance rate.

Respiratory

The following articles provide detailed information about:

You’ll get detailed information to help you get your best life insurance rate.

Brain and Nervous System

Nervous system conditions are covered in the following posts:

In the above guide, you’ll find detailed help for your condition.

General Medical Conditions

Several medical conditions do not fit traditional underwriting categories.

For those conditions, you’ll find detailed guides below.

Conditions such as:

- High Cholesterol Term Life Insurance

- COVID Life Insurance

- Alcohol Treatment History

- Naloxone Life Insurance

- Truvada Life Insurance

Tobacco and Nicotine Users

Everything you need to know, including how to qualify for non-tobacco rates when available.

We provide detailed information, including which companies are best for the following:

Whatever type of tobacco or nicotine products you use, you get the best advice from the above article.

Non-Medical Risks

Certain activities that you participate in may be considered high-risk from an underwriting standpoint.

Activities such as:

- Private Pilot

- Scuba Diving

- Mountain Climbing

- Motorized Racing

Our Avocation Underwriting section provides details.

No matter what type of avocation you participate in, life insurance options are available.

Get Your Best High-Risk Life Insurance Rate

With high-risk life insurance, it’s all about underwriting.

We wrote the following comprehensive guide to help you find affordable life insurance.

Underwriting topics reviewed in the above article include:

- What to do when you’ve been denied life insurance?

- How family history may affect your life insurance rates.

- What are table ratings, and how do they work?

- How flat extras work.

The biggest mistake made is going to the wrong company.

It’s the number one reason for a miserable experience, terrible rate, or even a letter of decline.

High-Risk Life Insurance Policies

When ratings are added to your policy, it makes sense to consider different types of life insurance to meet your needs best.

That’s where the following guide will help.

What Type of Life Insurance Should I Get?

In the above guide, you’ll find lots of great ideas for insurance planning, including detailed articles about:

- Term Life Insurance

- Universal Life Insurance

- Whole Life Insurance

- Accidental Death Insurance

- Guaranteed Issue Life Insurance

- Staggered Life Insurance (laddered life insurance)

This guide provides information about products, term lengths available, and the benefits and features of each type.

High-Risk Life Insurance Companies

No life insurance company is best for every health issue; many insurers want nothing to do with health conditions.

According to the CDC, millions of adults in the U.S. have severe health conditions that may affect their insurability.

Life insurers have strengths and weaknesses depending on the type of health issue, occupation, or activity.

For example, some companies are very good with diabetes, while others specialize in prostate cancer underwriting.

Risk-Free Shopping – You’ll receive the life insurance quotes you need to make an informed decision.

We’ll tell you everything you need to know, including which life insurance company is best for you and why they are best for you.

We provide you with accurate quotes from all companies.

Remember that there is never any pressure or obligation with our service.

Should you change your mind at any time, tell us to close your file.

And don’t forget that we also have high-risk companies for long-term care insurance and disability insurance.

FAQ

You have questions about high-risk life insurance, and we have the answers.

Final Thoughts

Whatever your high-risk situation, let us help you find the best life insurance options available.

There is never any pressure or obligation with our service.

Please request a quote today.