Are you worried about getting life insurance for a mental health condition? We can help!

This guide covers everything you need to know.

- Can You Get Life Insurance with a Mental Health Condition?

- Understanding the Underwriting Process

- Anxiety and Life Insurance

- Bipolar Disorder Life Insurance

- Depression and Life Insurance

- Types of Life Insurance for People with Mental Health Conditions

- The Application Process: What to Expect

- Life Insurance and Suicide

- Final Thoughts

Can You Get Life Insurance with a Mental Health Condition?

Yes, you can! Most people with a history of mental health conditions can qualify for life insurance.

It’s a common misconception that having an anxiety disorder or mood disorder diagnosis like depression or bipolar disorder will automatically disqualify you from coverage.

Examples of anxiety and mood disorders include:

While underwriting may be more complicated, high-risk life insurance companies do a great job of offering coverage to people with mental health issues.

Understanding the Underwriting Process

Life insurers review many factors, including your:

- Medical Diagnosis – What is your exact mental health condition?

- Treatment History – How is your mental health condition treated?

- Current Health – Do you take your meds and follow doctor’s orders?

Pro Tip:

If your physician has agreed to reduce or eliminate medications, or require less frequent appointments, make sure they document this in your records to avoid underwriting headaches!

The best life insurance rates go to those who proactively manage their health condition.

Anxiety and Life Insurance

The five main types of anxiety disorders that may affect life insurance underwriting include:

- Generalized Anxiety Disorder (GAD)

- Obsessive-Compulsive Disorder (OCD)

- Post-Traumatic Stress Disorder (PTSD)

- Social Anxiety and Panic Disorders

Underwriters review the type and severity of the anxiety disorder you were diagnosed with as well as these factors:

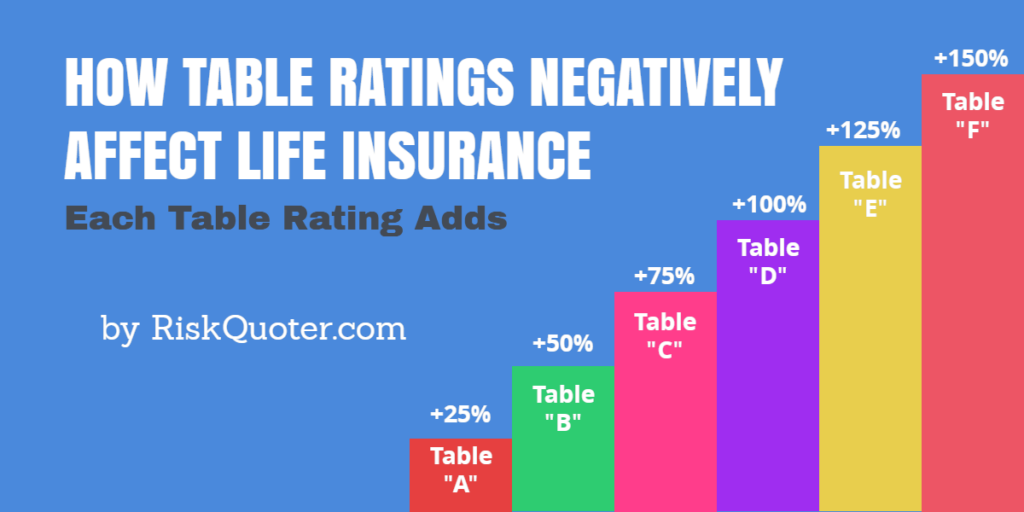

| Favorable Factors | Less Favorable Factors |

| More than 12 months since diagnosis | Less than 12 months since diagnosis |

| Taking 1-2 medications | More than 2 medications |

| Compliant with medications | Non-compliance with medications |

| Regular follow-up with physicians | Sporadic follow-up with physicians |

| Attends therapy as directed | Skips therapy, sporadic sessions |

| Stable family, work environment | Instability in family, work, etc. |

| No other psychiatric diagnosis | Psychiatric or personality disorders |

| Single episode | Multiple episodes |

| No suicide ideation or attempts | Suicide ideation or history of attempts |

Underwriters will review the severity of your condition, and the number of above favorable/unfavorable factors as part of underwriting.

Generalized Anxiety Disorder (GAD)

With GAD, underwriters look at the anxiety’s severity and your response to medication and therapy.

If your condition is mild and you respond well to medications and therapy, there is typically little (if any) negative effect on life insurance.

You may even qualify for the preferred best underwriting rate class with some life insurers.

Underwriters become concerned when the symptoms are more severe.

If your anxiety reaches the point where it causes lost time from work and hospitalizations, if you are not taking your medications or going to therapy, that becomes more difficult in underwriting.

Obsessive Compulsive Disorder (OCD)

With OCD, underwriters look at your medications and therapy compliance.

If your symptoms are controlled, and you have consistent follow-ups with your physician, the impact on life insurance rates is minimal.

Underwriting becomes concerned when obsessions and compulsions negatively affect your daily activities.

Panic Disorders

During a panic attack, you may have symptoms of:

- A pounding heartbeat

- Shortness of breath

- high blood pressure

- Shaking

- Sweating

The severity of your panic attacks, frequency, and recovery determine how it will affect your life insurance rate.

Post-Traumatic Stress Disorder (PTSD)

With PTSD, underwriters look at the underlying cause, current medical condition, and treatment history.

Lost time from work, failure to meet with your physician regularly, or any drug or alcohol abuse history will negatively affect underwriting.

Social Anxiety Disorder

Social phobias may affect life insurance if your current medical condition prevents you from participating in daily activities.

Working with a therapist, taking medications as directed, and improving over time are all helpful.

Bipolar Disorder Life Insurance

Bipolar Disorder 1 – This is classified as having at least one manic episode, and you may or may not have had previous episodes of depression.

This is the easier type of bipolar to insure.

Bipolar Disorder 2 – You have had at least one hypomanic episode.

Hypomanic episodes are similar to manic except that hypomanic are shorter in duration.

Life insurance underwriters look at Bipolar Disorder and will classify your Bipolar Disorder as either,

Mild bipolar, moderate bipolar, or severe bipolar disorder.

This classification is based on the severity of your bipolar disorder, medication for bipolar disorder, support network, suicide attempts, and hospitalizations.

Mild Bipolar Disorder – No lost time from work, no suicide attempts or hospitalizations, well-controlled on medication, and a good support network.

Moderate Bipolar Disorder – No more than one month of lost work time, no hospitalizations in the past 2-3 years, no suicide attempts in the past 2-3 years.

You may have some mood change history from medications and a good support network.

Severe Bipolar Disorder – Lost time from work for more than one month, history of dangerous behavior during manic periods,

There may be multiple hospitalizations or suicide attempts, major medications, lack of support network.

Depression and Life Insurance

When you’ve been diagnosed with depression, life insurers look at the following information.

- What was your exact diagnosis?

- When were you diagnosed?

- What treatment including medications do you receive?

- Are you compliant with doctor’s orders?

- Do you have any history of suicide ideation?

- Do you have any history of suicide attempts?

- Are you currently on disability?

- Have you filed for disability in the past due to depression?

We may have additional questions for you based on the above answers.

Remember that we work for you, not the life insurance companies. We will do everything possible to help you get affordable life insurance coverage.

Depression Guidelines by Company:

Some life insurance companies provide general underwriting guidelines for depression while others do not.

Here’s how some life insurers underwrite depression.

| Company | Underwriting Insights |

|---|---|

| Banner Life | Elite, Preferred Plus, and Preferred Rates1 No history of chronic mental illness or depression in 10 years. No history of treatment for drug or alcohol dependence. |

| Guardian | Preferred available depending on diagnosis, severity, and recovery. |

| Prudential | Preferred Best if mild depression, but no anti-psychotic or MAO inhibitor medications. |

| Pacific Life | Preferred available depending on diagnosis, severity and recovery. |

Mental health professionals may have used assessment tests such as the GAF or WHODAS to determine the impact of your health issues on everyday life and functioning.

GAF stands for Global Assessment Functioning and WHODAS stands for World Health Organization Disability Assessment Schedule.

GAF was an older assessment tool and the WHODAS is the current tool used by healthcare professionals.

GAF and WHODAS scores range from 0-100.

Make sure to use company-specific links to underwriting materials.

Types of Life Insurance for People with Mental Health Conditions

For most people, all types of life insurance are available.

Term life insurance for mental health conditions is readily available, with term lengths from 10-40 years depending on your age.

Permanent life insurance options include universal and whole life insurance policies.

Underwriting Tip

Some companies offer table shave or underwriting credit programs that give you better rates for universal life insurance rather than term life insurance.

With our service, we look at those options and will let you know how those options compare as sometimes the pricing may be similar to term life.

Guaranteed issue policies in small face amounts from $5,000 – $25,000 are available for age 50 or older.

Guaranteed issue is the last resort type of product when nothing else is available.

The Application Process: What to Expect

Here’s what happens when you first submit your quote request to RiskQuoter.

We’ll review the information you provide and we may have some additional underwriting questions for you.

For more mild health histories, we’ll provide quotes to you at that time.

If there are more significant health issues, we’ll use our quick quote process.

A quick quote allows us to shop your information to the best life insurance companies for mental health issues.

The benefit of the quick quote is it allows us to cover many companies quickly for you before you apply for life insurance.

When you apply for life insurance, companies will run searches of prescription databases and the Medical Information Bureau.

In addition, you’ll be asked if you have any other medical history such as cancer, diabetes, heart conditions, and more.

Life Insurance and Suicide

One of the most complicated and sensitive subjects we work with is any medical history related to suicide.

Underwriting falls into two broad categories – Suicide Ideation and Suicide Attempts.

Suicide ideation follows the underwriting rules above based on your exact diagnosis.

Underwriting for suicide attempts is based on the number of attempts and time since last attempt.

More than 2 attempts is a decline with companies.

We can help both.

The availability of life insurance depends on what happened, and where you currently are with treatment and recovery.

The following are general guidelines from companies that publish this info (not every company does)

| Prudential | Years Since Attempt | Rating |

| Single Attempt | Less than 3 | Decline |

| 3 – 9 years | Table B | |

| Greater than 9 years | Standard | |

| Two Attempts | Less than 5 | Decline |

| 5 – 9 years | Table 4 | |

| Greater than 9 years | Standard | |

| AIG-Corebridge | ||

| Single Attempt | 1 or Less | Decline |

| 1-2 | $5 flat 4 years | |

| 2-3 | $5 flat 3 years | |

| 3-5 | $5 flat 2 years | |

| More than 5 | Standard | |

| Two Attempts | 2 or less | Postpone |

| 2-3 | $5 x 4 | |

| 3-4 | $5 x 3 | |

| 4-5 | $5 x 2 | |

| More than 5 | Table 2 | |

| Pacific Life | ||

| Single Attempt | 1-2 years2 | Postpone |

| Banner Life | ||

| Single Attempt | 2 years | Postpone |

| Two Attempts | n/a | Permanent Decline |

Final Thoughts

Please take a few minutes to submit your quote request.

We’ll let you know exactly what to expect regarding underwriting and price.

There is never any pressure or obligation with our service.

Recent Articles: