Did you know that your life insurance may cost you 25% more if you have asthma and apply to the wrong life insurance company?

We’ve updated our asthma life insurance guide for 2024 to give you the most current and accurate information.

Understanding Asthma

Asthma is a chronic respiratory condition affecting 24.8 million Americans. It’s characterized by inflammation and narrowing of the airways (the tubes that carry air in and out of your lungs). This inflammation makes breathing difficult, leading to wheezing, shortness of breath, chest tightness, or coughing.

This article reviews how life insurance is affected by asthma types, severity, and control. We also provide our insurance company recommendations and price ranges for coverage.

How Asthma Impacts Life Insurance

Getting approved for life insurance with asthma ultimately depends on the following factors:

- Type of Asthma

- Asthma Severity and Frequency of Attacks

- Treatment and Long-Term Therapies

- Medical History

Type of Asthma

According to the American Lung Association, asthma is no longer viewed as one disease but rather broken down into various types of asthma.

- Allergic asthma

- Aspirin-induced asthma

- Cough-variant asthma

- Exercise-induced asthma

- Nighttime asthma

- Steroid resistant asthma

- Occupational asthma

Steroid Resistant and Occupational Asthma raise the greatest underwriting concern.

Getting better underwriting offers for people with allergy or exercise-induced asthma is sometimes possible.

Asthma Severity and Frequency of Attacks

Life insurance underwriting looks at the severity of your asthma as one of the most critical factors.

Insurance companies generally categorize asthma as:

- Mild Asthma

- Moderate Asthma

- Severe Asthma

Mild Asthma Life Insurance Underwriting

Individuals with mild asthma may experience occasional symptoms.

With mild asthma, you can get a “standard” rate all day long, BUT what you really want is a “preferred” rate.

From the 2024 company life insurance underwriting guidelines

Banner Life’s 2024 underwriting guidelines will consider preferred rates for “clients on two medications or less (well controlled).”

Transamerica’s 2024 underwriting guidelines, on the other hand, will consider a “standard – table 2” rating for mild asthma. In some cases, Transamerica may consider a “preferred” rate for those with an FVC>80% and the variability of FEV1 or PEF is <20%.

John Hancock will sometimes consider a “preferred” rate and possibly a “super preferred” rate for intermittent asthma. Mild cases can also receive a 50% rating at times.

Prudential may consider a preferred rate for people taking no more than one non-steroid medication.

Bottom Line – The right company is critical for mild asthma, so we always quick quote cases to all companies.

A preferred best rate may be available for those with exercise-induced asthma.

While physicians may classify your mild asthma as intermittent or persistent, underwriters treat both the same.

Moderate Asthma Life Insurance Underwriting

Individuals with moderate asthma may experience daily and nighttime symptoms.

With moderate asthma, “standard” or “standard plus” rates are common.

From the 2024 company life insurance underwriting guidelines

Prudential

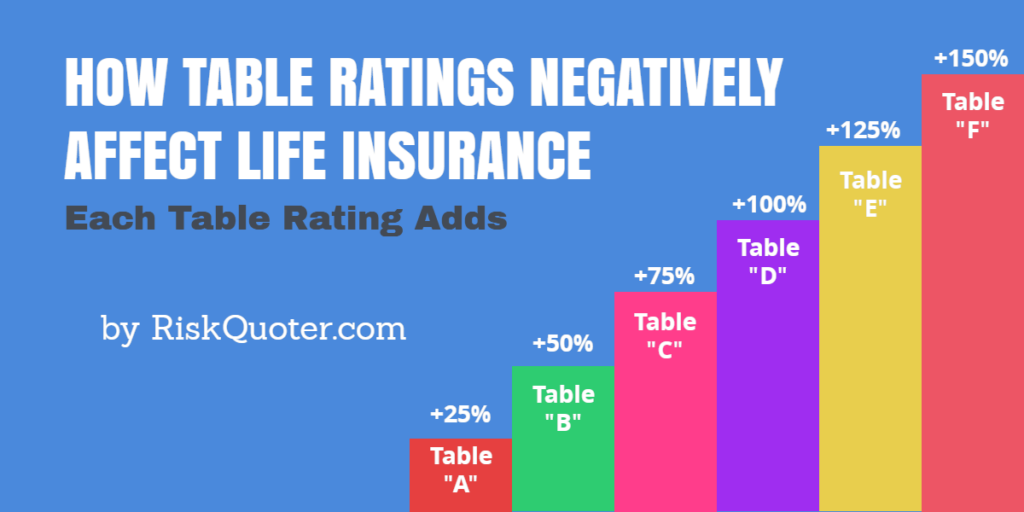

John Hancock – Typically add a Table 2 – Table 6 rating. Each table rating adds 25% to the price.

Brighthouse Financial’s underwriting guidelines indicate a Table 2 – Table 4 rating is likely.

Prudential underwriting indicates an outcome of “standard – Table 4” depending on individual factors.

Bottom Line – Every moderate case needs to be quickly quoted.

The above is just a sampling of underwriting. With our process, you’ll receive underwriting feedback from all competitive companies for asthma.

Severe Asthma Life Insurance Underwriting

With severe asthma, symptoms are continuous, and life insurance is on a case-by-case basis.

From the 2024 company life insurance underwriting guidelines

John Hancock – Severe asthma may be rated from Table 6 – Decline

Brighthouse Financial’s underwriting guidelines range from Table 6 – Decline.

AIG-Corebridge Financial – underwriting indicates range from Table 6 – Decline.

Prudential underwriting offers may range from Table 4 – Decline.

Keys to Success – The best way to help yourself is to follow your doctor’s orders, have regularly scheduled checkups, and take your medications.

Other health conditions have a significant negative effect on underwriting offers.

Asthma Treatment

Your treatment matters to life insurance underwriters.

If you are trying to get a “preferred” rate with a company, there are specific rules in place with some companies.

As mentioned earlier, Banner Life will consider preferred rates if your asthma is well-controlled and you take no more than two medications for asthma.

Prudential will only allow one non-steroid medication to be considered for a preferred rate with Pru.

John Hancock indicates that it will consider a preferred and even a super-preferred rate but does not indicate the criteria to qualify in its underwriting guidelines.

The Role of Medication and Treatment Compliance

How you manage your asthma is just as important as the initial diagnosis. Insurance companies will look at:

- The types of medications used

- Frequency of use

- Dosages taken

Medical History

Underwriting looks at your entire medical history in addition to asthma.

If you have a medical history of being heavier, cancer history, heart disease, sleep apnea, or diabetes history, underwriting becomes more complicated.

Hospitalizations for asthma can significantly negatively affect your life insurance rate, depending on the number of hospitalizations, duration of stay, treatment, and time since the last hospitalization.

Recent Articles:

Get the Best Life Insurance Table Rating for Your Situation

Top 10 Health Problems in America

Kidney Cancer Survivors – Life Insurance is Available!

If you’ve had kidney cancer and need life insurance, we can help you. Finding life…

Life Insurance for Throat Cancer Survivors

We specialize in high-risk life insurance underwriting for throat cancer survivors. While head and neck cancers…

Life Insurance After Colon Cancer: A Step-by-Step Guide

Addison’s Disease Life Insurance

If you have Addison’s Disease and need life insurance, let us help you. Our life…

Smoking and Asthma

Smoking cigarettes can significantly impact life insurance rates for asthmatics.

Life insurers hate underwriting people with asthma who also smoke.

It’s guaranteed that you will pay 50 – 200% more than non-smokers if companies will even consider coverage.

Guaranteed issue final expense policies may be the only option.

How to Find the Right Life Insurance Company When You Have Asthma

Work with an independent life insurance agent (hint, hint) who represents multiple companies and specializes in high-risk conditions like asthma.

We can give most people a ballpark pricing estimate in minutes.

That said, we quick quote all asthma cases for underwriting feedback.

Several life insurance companies understand the nuances of asthma and may offer more favorable rates or specialized programs.

These companies include include:

- AIG – Corebridge Financial

- Banner Life

- John Hancock

- Lincoln National

- Mutual of Omaha

- Protective Life

- Prudential

- Transamerica

The above are typically the best for asthma, but we’ll also contact other companies as sometimes you get lucky with an unexpected company.

Underwriting Questions for Asthma

Here’s what we need to know to quick quote your coverage:

- Your age at the time of diagnosis and your current age.

- The severity of your asthma – mild, moderate, severe

- Frequency of asthma attacks or exacerbations

- Hospitalizations

- Medications used and compliance with taking meds.

- Other health issues – obesity, heart, diabetes, lupus, etc.

- Tobacco use, if any.

Each life insurance company has underwriting guidelines, so comparing policies and rates from multiple insurers is crucial to finding the best coverage for your needs.

Frequently Asked Questions

You have questions about life insurance with asthma and we have the answers.

Remember that with our service, there is never any pressure or obligation. Our goal is to give you the information you need to make an informed decision about your life insurance.

Final Thoughts

Life Insurance with asthma is possible.

While asthma is a serious health condition, it shouldn’t prevent you from protecting yourself and your loved ones with life insurance.

Ready to secure the peace of mind that life insurance provides? Request a personalized life insurance quote today, and let us help you find the coverage that best fits your needs and budget.

Other Respiratory Conditions

In addition to asthma, we offer underwriting expertise for other respiratory conditions, such as COPD, Sarcoidosis, pulmonary nodules, and more.

Life Insurance with COPD

Chronic Obstructive Pulmonary Disease (COPD) affects nearly 16 million Americans, according to the National Institute of Health.

From an underwriting standpoint, COPD includes chronic bronchitis and emphysema.

While guaranteed issue policies are available, term life insurance is difficult to obtain if you have COPD.

When coverage is available, rates depend on the severity of COPD.

Underwriters look at your FEV1 and FVC reading results from a spirometry test, a type of pulmonary function test.

FEV1 – Forced Expiratory Volume in One Second measures the volume of your breath expelled in one second.

FVC – Forced Vital Capacity is the full volume of breath expelled in a full breath.

| COPD Severity | FEV1/FVC | Underwriting Rating |

|---|---|---|

| Minimal | Normal results | Standard rates |

| Mild | FEV1 60% or Higher FVC 70% or Higher | Table 2-4 rating |

| Moderate | FEV1 50% – 59% FVC 60% – 69% | Table 6 – 8 |

| Severe | FEV1 40% – 49% FVC 50% – 59% | Table 12 – Decline |

| Extreme | FEV1 less than 40% FVC less than 50% | Decline |

With COPD, the younger you are when diagnosed, the more difficult it is to get coverage.

Sarcoidosis

Life insurance for sarcoidosis is not very common, but when we have had clients, 99% of these applicants end up with Prudential.

Sarcoidosis is a lung disorder in which patients may have a chronic cough, difficulty breathing, abnormal chest X-rays, or Erythema Nodosa, a type of skin lesion.

Underwriting is based on the sarcoidosis stage, pulmonary function tests (PFT), and the time since reaching remission.

According to Prudential’s underwriting guidelines, possible outcomes are:

| Sarcoidosis Stage | Remission 6 – 24 months | Remission More Than 2 Years |

| Stage 1 | Standard Rate Plus 50% | Standard Rate |

| Stage 2 | Standard Rate Plus 125% | Rate Based on PFT Results |

| Stage 3 | Decline | Rate Based on PFT Results |

| Stage 4 | Decline | Decline |

Active sarcoidosis is a decline, except for guaranteed issue policies.

Pulmonary Nodules

Life insurance for pulmonary nodules depends on several factors.

Benign pulmonary nodules may be insurable;

Your application for term, universal, or whole life will be declined if the diagnosis is anything else. Guaranteed issues and accidental coverage are available.

For benign pulmonary nodules 4mm or less in size, life insurance is available 6-12 months after your radiologist has determined that the nodule is benign and no other treatment is required.

Whatever your medical condition is, please submit your request for quotes.

We’ll do our best to find affordable life insurance for you.